Introduction:

Say you started a Rs.15,000 monthly SIP in February 2007, intending to buy a house in 2020. By February 2020, as per an SIP calculator, you would have collected a corpus of around Rs.48,08,995 with 10% interest, right? Since mutual funds work closely with the market, given the pandemic in 2020, the SIP would have shrunk to at least half due to declining markets.

Just like that, years’ worth of discipline can be shredded because of uncertainties, which makes it essential to plan your SIP disciplines and think of the reward harvesting phase with plans like SWP, especially when factoring in inflation and adjusting for life-stage investing.

What is SWP in mutual funds? How does it help? Let’s understand.

What is SWP?

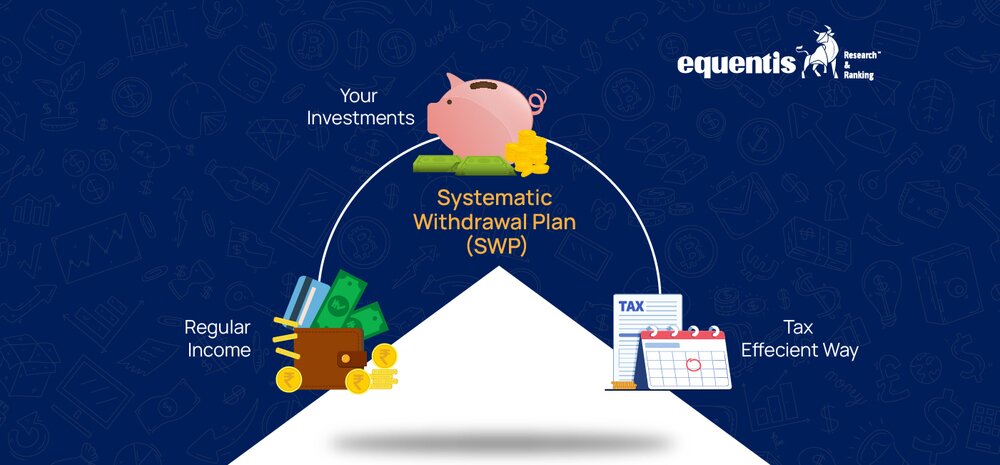

A Systematic Withdrawal Plan (SWP) lets you regularly withdraw a fixed amount from a mutual fund. It gives flexibility to decide how much and how often to withdraw. You can also withdraw only the returns, leaving your invested capital untouched. The required units are sold from the portfolio on the selected date, and the money is transferred to your account.

How Does SWP Work?

Let’s understand the process better with an example.

Say you own a mutual fund worth Rs.10,00,000, and its NAV is Rs.15. You opt for an SWP to receive Rs.6000 monthly. In the first month, the mutual fund house will sell 400 units (6000/15) and release Rs.6000 as committed.

Next month, say the market took a downturn, and the NAV dropped to Rs.12. So, the fund house will sell 500 units this month and release Rs.6000. In the third month, say the market bounced back and took NAV to Rs.20. This time, the number of units sold will be 300.

Each withdrawal reduces your total units. However, with a higher NAV, fewer units are redeemed to meet your cash needs. On the flip side, if the NAV drops, more units are sold for the same amount.

NAV fluctuates because it is connected to the securities market, and sometimes, this move can be drastic due to certain market conditions. So, how can SWPs be planned to give maximum benefit and mitigate the effects of possible volatility?

Things To Consider When Setting an SWP:

When planning an SWP in mutual funds, you can look at the following two factors to begin with-

Setting the Right Withdrawal Amount

Your withdrawal should always be less than your investment’s rate of return. This keeps your corpus growing while giving you regular payouts. To decide the amount, consider:

- Duration of Investment: Long-term goals like retirement need a different approach than short-term goals like education or home purchases.

- Income Needs: Your withdrawal should match your lifestyle or goal-specific requirements.

- Compounding Before Withdrawals: Delaying withdrawals allows your funds to compound, increasing wealth and ensuring funds last longer. So try to keep the withdrawals as close to maturity as possible.

Understanding Market Volatility and Investment Choices:

Pairing SWP with smart investments ensures smoother withdrawals. Your portfolio mix plays a big role here.

- Diversified Portfolio: For stability, 50-60% of your portfolio can be in stocks and mutual funds, with the rest in bonds, gold, or other safe options. This balances growth and risk, ensuring steady returns and liquidity.

- All-Equity Funds: For aggressive growth, initially keep withdrawal limits low. Allowing funds to compound for 5-7 years before starting withdrawals can significantly enhance your corpus.

Why Should One Consider SWP?

SWP Prevents Impulsive Exits:

Market volatility often triggers panic exits as a goal approaches. These may temporarily protect your funds but can fall short of your target corpus. An SWP offers a balanced approach by enabling gradual withdrawals instead of a lump sum. Only a small portion is redeemed during market dips, allowing the remaining investments to recover when markets rebound.

This strategy avoids timing mistakes, much like SIPs during accumulation. SWPs also provide regular returns, giving emotional reassurance while weathering market fluctuations. Since recoveries often span 12-24 months, SWPs help maintain growth potential without disrupting long-term goals.

Rupee Cost Averaging:

Selling units in installments through SWP helps avoid market timing risks. Fewer units are redeemed when markets are high and more when markets are low. It balances out the cost and protects against losses compared to a lump sum withdrawal during a market downturn.

Offers Certainty and Flexibility:

SWPs provide steady cash flow to meet expenses, offering fixed withdrawals monthly or quarterly by redeeming units. Unlike dividend plans like Income Distribution Cum Capital Withdrawal (IDCW), where payouts depend on fund profits, SWPs ensure consistent income until the corpus depletes. They also outperform insurer pension plans by letting investors set their payouts. Ideal for retirees, SWPs streamline cash flows during retirement and can generate secondary income for others.

Tax Efficient Option

With an SWP, tax is charged only on the capital gain, not the full withdrawal amount. For instance, if you withdraw Rs.5,000 from 1,000 units of a fund bought at Rs.100 NAV, and the current NAV is Rs.102, you redeem 49.02 units. You pay tax only on Rs.98, the gain.

For equity funds, gains up to Rs.1 lakh annually are tax-free. For debt mutual funds, short-term gains are taxed per your slab rates, and long-term gains (more than 3 years) are taxed at 12.5%. Compared to taxable FD interest or mutual fund dividends, SWPs significantly lower the tax burden.

Timing the Exit in SIPs

Exiting SIPs at the goal date can expose investments to market risks. An SWP offers better control and flexibility by allowing adjustments to withdrawal amounts and frequency.

Many AMCs provide a top-up feature to combat SWP with inflation or reduce withdrawals based on cash-flow needs. Unlike dividend plans, pension plans, or FDs, an SWP lets you easily modify monthly withdrawals to suit requirements or meet unexpected expenses.

Capital Preservation:

SWP lets you withdraw funds systematically, keeping most of your investment intact for long-term growth. This ensures your portfolio stays invested and continues to grow over time.

Bottomline:

An SWP may not guarantee you reach your target amount, but it helps manage risk. It ensures you don’t sell at the bottom, though you may miss out on selling at the peak. Perfect timing is only possible in hindsight. The SWP smoothens extreme outcomes in both directions, making it a practical option for many investors. The key idea is minimizing regret on the downside while leaving room for potential upside.

Overall, a SWP offers a balanced approach that works for most people. To make it work for you, tailor it to your goals and consult a registered stock market advisory before making any decisions.

Disclaimer Note: The securities quoted, if any, are for illustration only and are not recommendatory. This article is for education purposes only and shall not be considered as a recommendation or investment advice by Equentis – Research & Ranking. We will not be liable for any losses that may occur. Investments in the securities market are subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, membership of BASL & the certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

FAQ

Who should opt for SWP?

SWP in mutual funds is a good option for investors who need a steady income, like retirees, pre-retirees, or those with financial obligations. It’s also suitable for those in higher tax brackets or looking for capital protection. If you fall into any of these categories, consider investing in the best mutual fund for SWP.

Can I stop the SWP anytime

Yes, you can stop an SWP anytime. With an SWP plan, investors can decide the amount, frequency, and withdrawal date. This option allows them to pause the plan or add more investments.

What is an SWP interest rate?

SWP interest rates refer to the returns from mutual funds, but they don’t offer fixed rates. Instead, your returns depend on how the mutual fund performs. These returns can vary each year and are not guaranteed. However, over the long term, mutual funds (especially equity funds) tend to provide higher returns than bank deposits.

I’m Archana R. Chettiar, an experienced content creator with

an affinity for writing on personal finance and other financial content. I

love to write on equity investing, retirement, managing money, and more.