Let’s start with some Good News; then move to the …Great News.

After struggling for over a week in Red, the Indian markets recouped to Green on the closing bell yesterday. What changed?

There has been neither a significant change in the economy nor a positive update on the Russia-Ukraine war. In fact, Ukraine has declared an air alert in Kyiv as the war continues. In our opinion, it’s the very nature of the markets that revived it from a week’s slumber. Sensex gained over 1,000 and NIFTY jumped more than 300 points on the back of exit polls suggesting wins across UP and Manipur for the BJP.

To effectively invest your money into equities amid such turbulent times, subscribe to our 5 in 5 Wealth Creation Strategy here.

Now, let us come to the Great News. In today’s article, we will learn about FPIs or Foreign Portfolio Investors.

If you are keeping up with the media reports, you may have come across the following headlines,

“FIIs pull out more than $29 bn in FY22 amid high valuations, US Fed rate hike fears, and geopolitical tensions“

“FIIs outflow shoots past Rs. 2 Lakh crore since October, but DIIs offer a balance“

“Foreign Investors likely to continue pulling out funds“

Of course, the headlines alone are scary. But is the matter really grave? Should you worry if foreign investors are pulling their money from Indian equities?

We will answer these questions here but before that know who FPIs are.

Know FPIs

Foreign Portfolio Investors or FPIs are foreign entities governed by the market regulator SEBI. They are allowed to invest in various financial assets categories, including shares of listed companies, non-convertible debentures, government securities, mutual funds, and other asset classes.

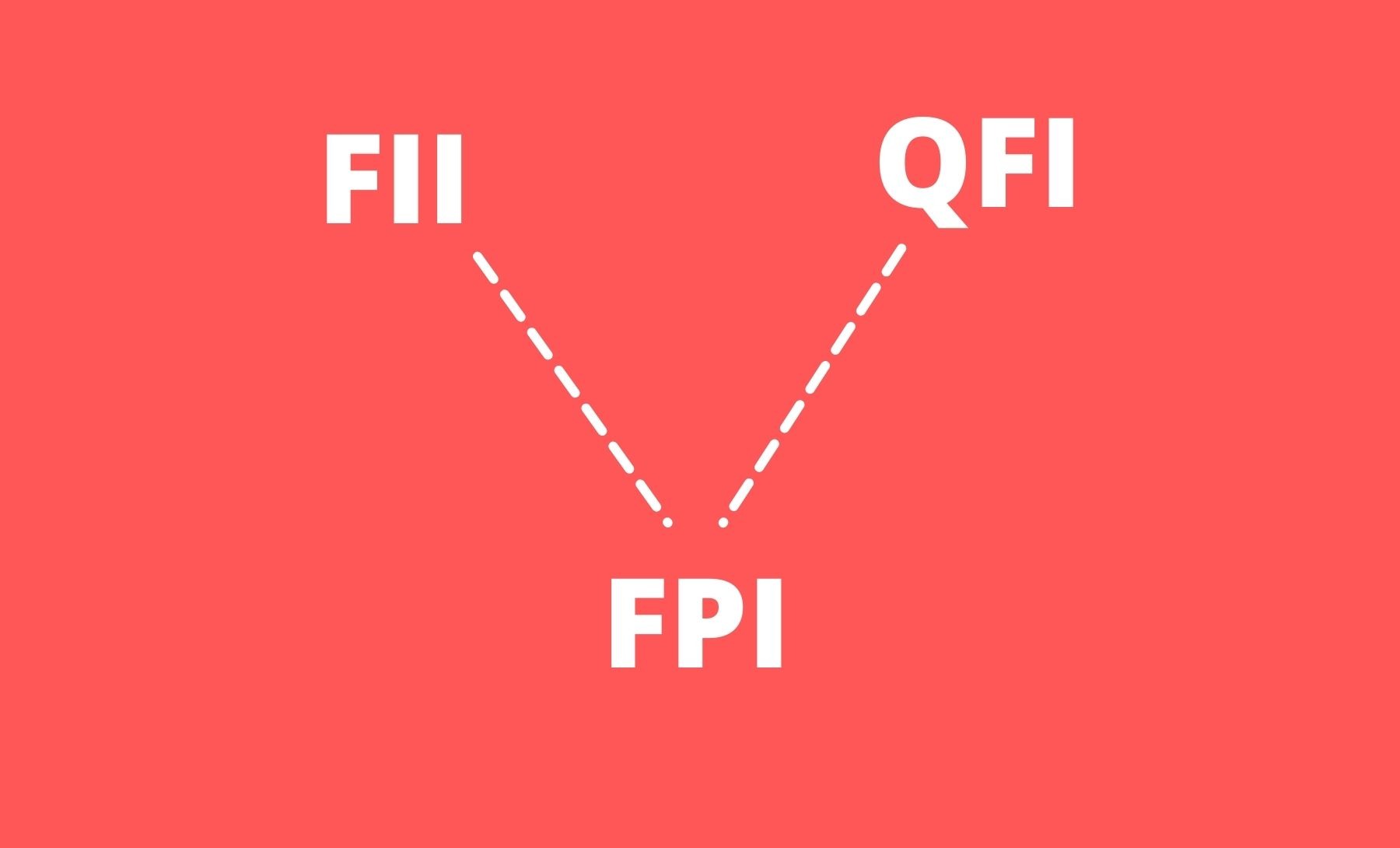

FPI regime is a harmonized route for foreign investment in India. FIIs (Foreign Institutional investors) and QFI (Qualified Foreign Investors) are together called FPIs. However, many use the terms FIIs and FPIs interchangeably.

Categories of FPIs

According to a leading consulting firm PwC, there are three categories of FPIs. Look at the chart below to understand these categories better.

FPIs presence in the Indian markets

FIIs (FPIs since 2014) were allowed to invest in India since 1992. As the rules got amended, authorities open other investment channels such as the corporate debt market (1995) and Government securities (1997) to FPIs. Over the years, FPIs made a significant amount of investments in the country, especially in equities of listed companies through both primary and secondary markets. Per the CDSL website, FIIs invested an enormous sum of Rs. 2.74 lakh crore in FY21, a record high till today. If you were to go by the numbers, only 3 out of 20 years the FPIs have been net sellers in the Indian equity markets.

Should you worry if FPIs sell today?

The simple answer is no.

Yes, the FPIs have pulled money from the Indian equities in FY22. Per the CDSL website, they have sold equities worth Rs. 1.36 Lakh crore as of March 9, 2022. But this does not mean they are going away from the Indian stock markets.

There is no one size fit for FPIs. Like any other investor class, they have different horizons, objectives, and investment strategies. For instance, Pension funds have a very long-term horizon (decades) but Hedge funds & AIF have a short-term horizon (3-6 months).

Many FPIs take self-canceling positions in equities of various regions, categories, segments, countries, etc. They leverage on the short-term trading opportunities, which do not define their fundamental view on a country, region, stock, etc. They just complete their assigned tasks – buy and sell.

Moreover, FPIs alter their buy and sell activities based on the asset allocation ratio. They take strategic calls on shifting from equities to debt or from secondary to primary markets or from India to other countries.

Thus, don’t panic when read or hear a sensational headline talking about FPIs pulling money from the markets. We recommend you analyze the reasons behind the selling, whether it’s because of a structural change or just trading strategies.

If you think this is a lot to do, we can help you out with your equity investment needs. Subscribe to our 5 in 5 Wealth Creation Strategy to begin your wealth creation journey today.

Read more: How Long-term investing helps create life-changing wealth – TOI.