Introduction:

Imagine you are on a business trip, staying at a luxurious hotel, and dining at high-end restaurants. You swipe your card confidently, knowing there’s no fixed credit limit — just flexible spending power. This is the advantage a charge card can offer. On the other hand, a credit card would allow you to split those expenses into manageable monthly payments, providing flexibility when cash flow is tight.

Both charge cards and credit cards serve unique financial purposes. Understanding their differences is crucial to managing your finances effectively. While both enable cashless transactions, they vary in repayment rules, spending limits, and fees. Let’s break down these differences to help you make the right choice.

What is a Credit Card?

A credit card is a payment tool that allows users to borrow money up to a predetermined credit limit. Cardholders can make purchases and choose to repay the balance in full or over time. If the entire amount isn’t paid by the due date, interest is charged on the remaining balance.

Key Features of Credit Cards:

- Credit Limit: Each card comes with a spending limit based on your credit profile. The limit is determined by your credit history, income, and repayment behaviour. For instance, individuals with a strong credit score may receive a higher limit, enabling them to manage large expenses like travel, electronics, or emergencies.

- Flexible Repayment: Credit cards offer the flexibility to pay the full bill or just a minimum amount by the due date. However, any unpaid balance accrues interest. For example, if you make a large purchase, you can break the payment into smaller installments to manage cash flow effectively.

- Interest Rates: Interest is typically charged on overdue amounts and cash advances. Rates vary based on the card type and provider, often ranging from 24% to 48% per annum. Timely payments are crucial to avoid accumulating high-interest costs, which can grow quickly over time.

- Rewards Programs: Credit cards frequently offer rewards like cashback, airline miles, or shopping points. For example, spending on fuel may earn extra cashback, while international travel purchases could provide bonus points redeemable for flights or hotel stays.

Picture this: You are hosting a family gathering at a fine-dining restaurant, followed by shopping for last-minute gifts. You confidently swipe your charge card, knowing there’s no fixed spending limit to worry about. Alternatively, a credit card would allow you to divide those expenses into manageable monthly payments, giving you better control over your budget.

What is a Charge Card?

A charge card is a type of payment card that requires the full balance to be paid off every billing cycle. Unlike credit cards, charge cards don’t allow users to carry forward debt to the next month. These cards are typically offered to individuals or businesses with strong credit profiles.

Key Features of Charge Cards:

- No Pre-set Spending Limit: Charge cards often have no fixed credit limit, providing greater flexibility for high-value transactions. However, this doesn’t mean unlimited spending; transactions are approved based on your spending patterns, financial behaviour, and credit history. This flexibility can be particularly useful for corporate expenses, luxury shopping, or urgent high-cost transactions.

- Full Balance Repayment: Users must pay the entire bill by the due date. Missing payments can result in hefty penalties or card suspension. This structure encourages financial discipline and ensures that cardholders maintain control over their expenses.

- Annual Fees: Charge cards usually have higher annual fees compared to credit cards, often justified by premium rewards and perks. These fees may cover luxury benefits like global concierge services, travel insurance, or elite access to airport lounges.

- Exclusive Benefits: Charge cards often come with superior reward programs, including higher cashback rates, hotel upgrades, complimentary memberships, and elite travel perks. For example, some charge cards may provide personalised travel planners, premium dining privileges, and VIP customer support.

- Ideal for High Spenders: Charge cards cater to individuals or businesses with significant monthly spending capacity. Their flexibility and premium benefits make them a preferred choice for entrepreneurs, frequent travellers, and luxury spenders.

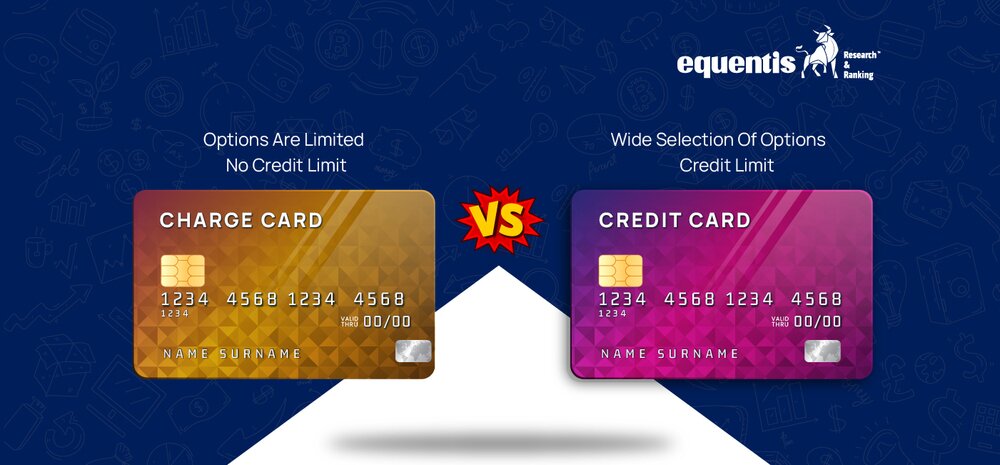

How is a Charge Card Different From a Credit Card?

The difference between the two are mentioned below:

| Feature | Charge Card | Credit Card |

| Spending Limit | Charge cards have no pre-set spending limit, meaning there’s no fixed cap like a credit card. However, this doesn’t imply unlimited spending. The approval of transactions depends on factors such as spending patterns, income profile, and financial behaviour. This makes charge cards ideal for those with fluctuating expenses or frequent high-value transactions. | Credit cards come with a fixed credit limit that restricts spending within a defined range. The credit limit is determined based on the user’s credit score, income, and repayment behaviour. Credit limits provide better spending control but may limit flexibility for large transactions. |

| Repayment | Charge cards require full payment of the outstanding balance by the due date. Failure to pay in full can lead to severe penalties, including card suspension. This payment structure promotes financial discipline, ensuring users manage their spending responsibly. | Credit cards offer flexible repayment options. Users can choose to pay the total outstanding amount, the minimum due, or a partial amount. Unpaid balances are carried forward with interest, giving users the flexibility to manage cash flow but at the risk of higher debt accumulation. |

| Interest Charges | Charge cards do not impose interest charges since balances must be cleared in full every month. This eliminates the risk of mounting interest expenses, but requires disciplined financial management. | Credit cards accrue interest on unpaid balances. The interest rate often ranges between 24-48% annually, making it costly if balances are left unpaid for extended periods. Timely repayments are essential to avoid accumulating excessive interest charges. |

| Late Payment Consequences | Missing payments on a charge card results in severe penalties. Card suspension is common, and users may lose access to premium services until the balance is cleared. This stringent approach encourages responsible financial behaviour. | Late payments on credit cards result in late fees and interest accumulation. While these penalties are generally less severe than charge cards, consistent delays can damage your credit score and limit future borrowing capacity. |

| Rewards & Benefits | Charge cards typically provide superior rewards, including premium travel perks, VIP lounge access, personalised concierge services, and hotel upgrades. These exclusive benefits cater to individuals with higher spending power. | Credit cards also offer rewards, but the value and variety may vary. Some cards focus on cashback, while others prioritize travel, shopping, or lifestyle discounts. Benefits depend heavily on the card type and provider. |

| Annual Fees | Charge cards generally have higher annual fees to compensate for their premium perks. The fees are often justified by the enhanced services and luxury privileges that charge cards provide. | Credit card fees vary widely. Entry-level cards may have zero annual fees, while premium cards offering extensive benefits may charge higher fees. Choosing the right credit card depends on your spending habits and lifestyle preferences. |

Disclaimer Note: The securities quoted, if any, are for illustration only and are not recommendatory. This article is for education purposes only and shall not be considered as a recommendation or investment advice by Equentis – Research & Ranking. We will not be liable for any losses that may occur. Investments in the securities market are subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, membership of BASL & the certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

| Who Can Benefit the Most from a Charge Card? Charge cards are best suited for individuals and businesses with specific financial habits and requirements. Here’s a detailed breakdown of who should consider using a charge card: 1. Individuals with Strong Financial Discipline: A charge card requires you to pay off the entire balance every month. This means it’s ideal for people who are diligent about managing their finances and consistently pay their bills on time. If you follow a strict budget and avoid overspending, a charge card can help streamline your expenses without accumulating debt. 2. Those Looking to Avoid Interest Charges: Unlike credit cards, charge cards don’t have a revolving credit facility — meaning you can’t carry forward an unpaid balance. For individuals who prefer to clear their dues fully each month, this feature eliminates the risk of paying hefty interest charges. 3. Frequent Travelers and Luxury Spenders: Charge cards often come with exclusive perks designed for high-end lifestyles. If you frequently travel or enjoy premium experiences, you can benefit from: Airport lounge accessTravel insurance coverageReward points on luxury spendingConcierge services for bookings and reservations These benefits make charge cards particularly appealing to those who enjoy elevated experiences and want to maximise their spending value. 4. Business Owners with High Spending Needs: For entrepreneurs and professionals who incur significant monthly expenses, charge cards provide flexible spending limits. This can be especially useful for managing business-related costs such as inventory, client entertainment, or travel expenses. With no pre-set spending cap, charge cards offer the flexibility required for businesses with fluctuating cash flow. 5. Individuals Seeking Enhanced Expense Management: Charge cards often come with advanced expense tracking tools, helping users categorise and analyse their spending patterns. This feature is particularly valuable for those looking to improve their financial planning and budgeting strategies. In essence, a charge card is best suited for those who are confident in their ability to manage money responsibly, pay off balances in full each month, and value exclusive benefits that align with their lifestyle or business needs. |

In conclusion, both charge cards and credit cards have their advantages. A charge card offers enhanced benefits for disciplined users, while a credit card provides flexibility for those who may need to manage cash flow over time. Understanding these differences can help you choose the ideal payment tool for your financial needs. |

Related Posts

Disclaimer Note: The securities quoted, if any, are for illustration only and are not recommendatory. This article is for education purposes only and shall not be considered as a recommendation or investment advice by Equentis – Research & Ranking. We will not be liable for any losses that may occur. Investments in the securities market are subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, membership of BASL & the certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

FAQ

Are charge cards better than credit cards?

Charge cards are better for disciplined spenders seeking premium perks. Credit cards are preferable for those needing flexible payment options.

Can I build credit with a charge card?

Yes, consistent on-time payments on a charge card can improve your credit score, just like a credit card.

Are charge cards accepted everywhere?

Charge cards are generally accepted widely, but acceptance may vary in smaller establishments.

What happens if I miss a charge card payment?

Missing a payment may result in significant penalties, and your account may be restricted until the balance is cleared.

I’m Archana R. Chettiar, an experienced content creator with

an affinity for writing on personal finance and other financial content. I

love to write on equity investing, retirement, managing money, and more.